Year-One of Analytics – A Crucial Juncture

The Dark Knight – by Roopam

I am a big fan of the graphic novel – Batman: the Dark Knight Returns – by Frank Miller. I almost lost my faith in Batman after watching the utterly ridiculous television series from the 60s – based on camp aesthetic. Batman was more of a joker in that TV series. I must thank Frank Miller for bringing darkness back to Batman and reinstating my faith in the caped crusader. Recently, I read another Batman masterpiece by Frank Miller caller ‘Year One’. The book captures the beginning of Bruce Wayne’s successful career as Batman. The year one is about performing several things right for a lasting and rewarding journey as the superhero.

This has made me think about the year one of advanced analytics journey for an organization. I have been lucky in my career to be part of a few such initiatives, including designing and setting up advanced analytics center-of-excellence. The year one is of particular importance since it paves the way for an exciting and rewarding analytics journey for an organization. The primary purpose of Analytics is to positively influence the key-performance-indicators (KPIs) of the organization through intellectual rigor. Eventually, analytics results need to monetize to measure the impact on the financials of the organization.

Advanced-Analytics-1.0 Solutions for loan portfolios

Shylock – a Jewish moneylender – from Shakespeare’s The Merchant of Venice – by Roopam

A few months ago while having a cup of coffee in a restaurant I eavesdropped on a conversation between a boy and a girl. Both the kids were not more than 10 years old. There was a delicate negotiation of chocolates taking place between them. The girl with a handful of chocolates was ready to offer a chocolate to the boy with the condition that he will return three chocolates to her the next day. The boy was adamant about returning just two and no more. I could not wait there longer to learn the outcome of the negotiation. However, I could understand the reason why lending is referred to as the second oldest profession after prostitution. The concept of lending and earning some interest out of the principal in the near future is something kids could decipher.

In this article, I have compiled a list of seven advanced analytics solutions for lending firms to initiate an advanced analytics journey. I am referring to these Analytics solutions version-1.0 to emphasize that there lie exciting times, strategic thinking and analytical rigor in the subsequent years to follow the year-one.

A simple Cash-Flow Model for Loan Portfolios

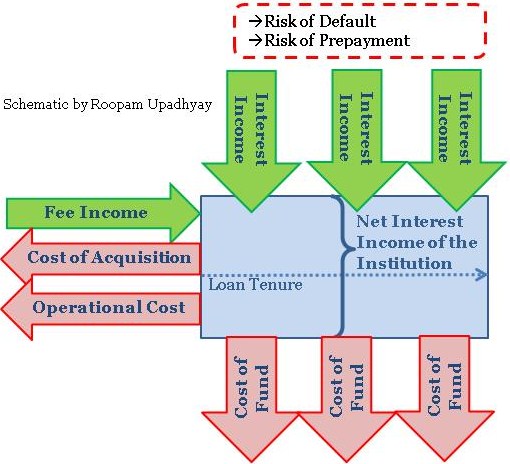

Before discussing the analytics solutions in some detail, let us create a simplistic cash-flow model for a lending firm. There are a couple of reasons for creating this cash flow model, firstly, to understand the primary functioning of a lending firm. Moreover, we would like to link our solutions and their impact on the overall monetary engine of the institution. A very simplistic model for a loan will have the following components:

Schematic of cash flow for loan portfolios

1. Cost of Acquisition: the cost incurred by the financial institution to procure a customer

2. Fee Income: the fees that the institution charges to the customer to process her loan application

3. Operational Cost (application): the operational cost incurred by the institution while processing an application form. The cost of acquisition and operational cost is covered to some extent by the processing fees.

4. Interest Income: income that the institution earns through monthly installments (EMIs)

5. The cost of Fund (interest expense): the money that the institution has lent out to the borrowers is received from the equity holders and debtors. The predominant sum usually comes from the debtors. The premium expected on the fund by the investors is the cost of fund.

6. The probability of Loss / Default: the primary source of risk in the lending business is borrowers’ inability or unwillingness to repay the loans. This risk is also known as credit risk.

7. The probability of Prepayment: another risk that affects a loan portfolio is the prepayment risk, which creates a mismatch in cash flow. This is common for home loans because of their long tenure. The primary reason for this risk is principal’s balance transfer (BT) to other lenders.

7 Advanced-Analytics-1.0 Solutions for loan portfolios

I would propose the following solutions, as a part of Analytics 1.0, for lending firms in the year-one of the analytics journey.

1. Customer Segmentation

2. Cross / up sell (Customer onboarding)

3. Application / credit scorecard

4. Behavioral Scorecard

5. Loan-loss-provisioning model

6. Prepayment / customer churn model

7. Customer/ portfolio value

We will explore these solutions in some details in the subsequent articles of this series. See you soon!

Sign-off Remark

I wish your year-one of analytics results in a glorious and lasting journey as it did for the legendary dark knight. Trust me they all have tremendous potential!

I liked Batman since childhood and to this day.